Portugal Housing Tax Package: Key Considerations for Private Clients

Decree-Law 97/2026, published on 20 May 2026, introduces a set of tax measures designed to stimulate the supply of residential housing in Portugal.

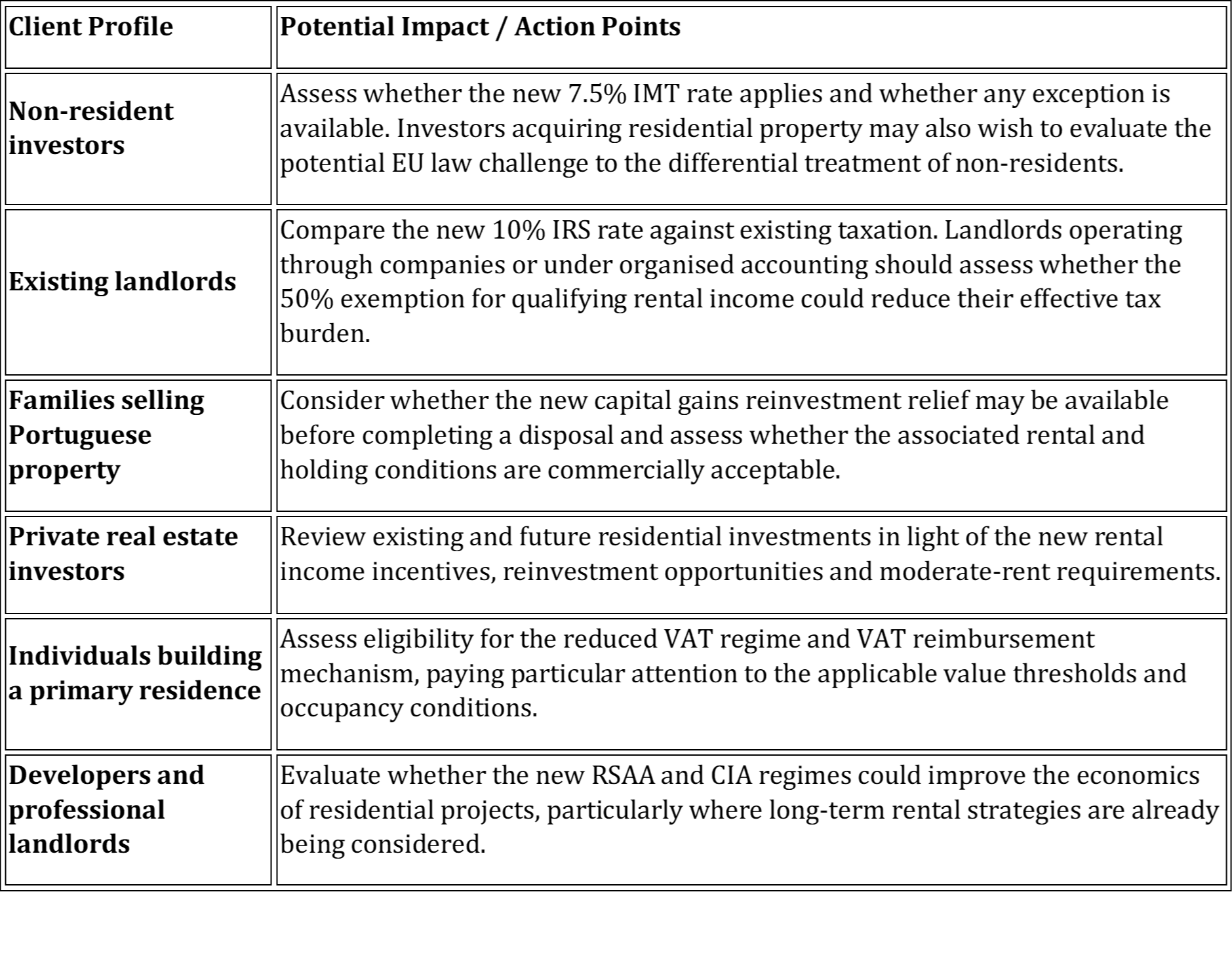

While many of the measures are primarily aimed at developers and institutional investors, several provisions directly affect private clients, particularly non-resident purchasers, landlords and families holding or intending to hold Portuguese real estate.

The package combines tax incentives with a significant number of eligibility conditions, investment commitments, rent limitations and monitoring requirements, making several of the measures restrictive in practice. As a result, the practical attractiveness for private investors will likely be rather limited and depend on the evolution of the implementation requirements.

The key measures affecting private clients include:

Introduction of a 7.5% real estate transfer tax rate (“IMT”) for non-resident purchasers of residential property;

New capital gains reinvestment relief for individuals investing in qualifying residential rental property;

Reduced taxation of rental income derived from moderate-rent leases;

Reduced 6% VAT and VAT reimbursement mechanisms for qualifying residential construction projects.

In this briefing, we review the principal measures affecting private clients and highlight some of the practical considerations that should be taken into account before relying on the new incentives.

1. New Transfer Tax Rules for Non-Resident Buyers

Under the proposed rules, non-resident purchasers of residential property would generally be subject to an increased flat 7.5% IMT rate, without access to the ordinary progressive rates available to Portuguese tax residents. For acquisition prices below €1,150,853, the higher 7.5% IMT rate would not apply where:

the purchaser is already Portuguese tax resident;

the purchaser becomes Portuguese tax resident within two years of the acquisition; or

the purchaser places the property into qualifying affordable residential rental use (currently expected to correspond to monthly rents below approximately €2,300).

Interestingly, the exception from the higher rate also applies where the purchaser has previously qualified as Portuguese tax resident at any point in time. This element of the new law raises material compatibility concerns under EU law, particularly in light of Article 63 TFEU (free movement of capital), which extends to cross-border real estate investments.

Case Study

Mark is a United States tax resident acquiring a residential property in Portugal as a secondary residence for €800,000. Based on the new law, Mark will be liable to:

IMT (Transfer Tax) at 7.5%: €60,000

Stamp Duty at 0.8% (separate one-off tax due on acquisition): €6,400

Total acquisition taxes payable at completion: €66,400

Under the ordinary resident IMT rules, the tax burden for an acquisition of a secondary residence at the same value would generally be materially lower than the combined tax 8.3% on purchase price. By way of illustration, the ordinary rates could result in IMT of Mark being approximately €48,000, generating a differential of approximately €12,000.

Kore Take

Kore Partners believes there are credible grounds to argue that the application of the higher IMT rate exclusively to non-resident purchasers may be incompatible with Article 63 of the Treaty on the Functioning of the European Union (which extends to third countries, such as the US in the case of Mark). If such incompatibility were ultimately confirmed, affected taxpayers could potentially seek reimbursement of the excess IMT paid and compensatory interest from the Portuguese State.

It is expected that the Portuguese Tax Authorities would not voluntarily accept such refund claims, meaning that arbitral proceedings would likely be required. Given the EU law dimension of the issue, it is also conceivable that a Portuguese arbitral tribunal could submit a preliminary reference to the Court of Justice of the European Union regarding the compatibility of the regime with EU free movement principles.

The new 7.5% transfer tac rate becomes the default regime applicable to most non-resident investors acquiring residential property in Portugal, unless they are prepared either to relocate their tax residence to Portugal or to place the property into qualifying affordable residential rental use subject to rental limitations. Kore Partners is available to analyse individual acquisition structures and advise the request for a refund.

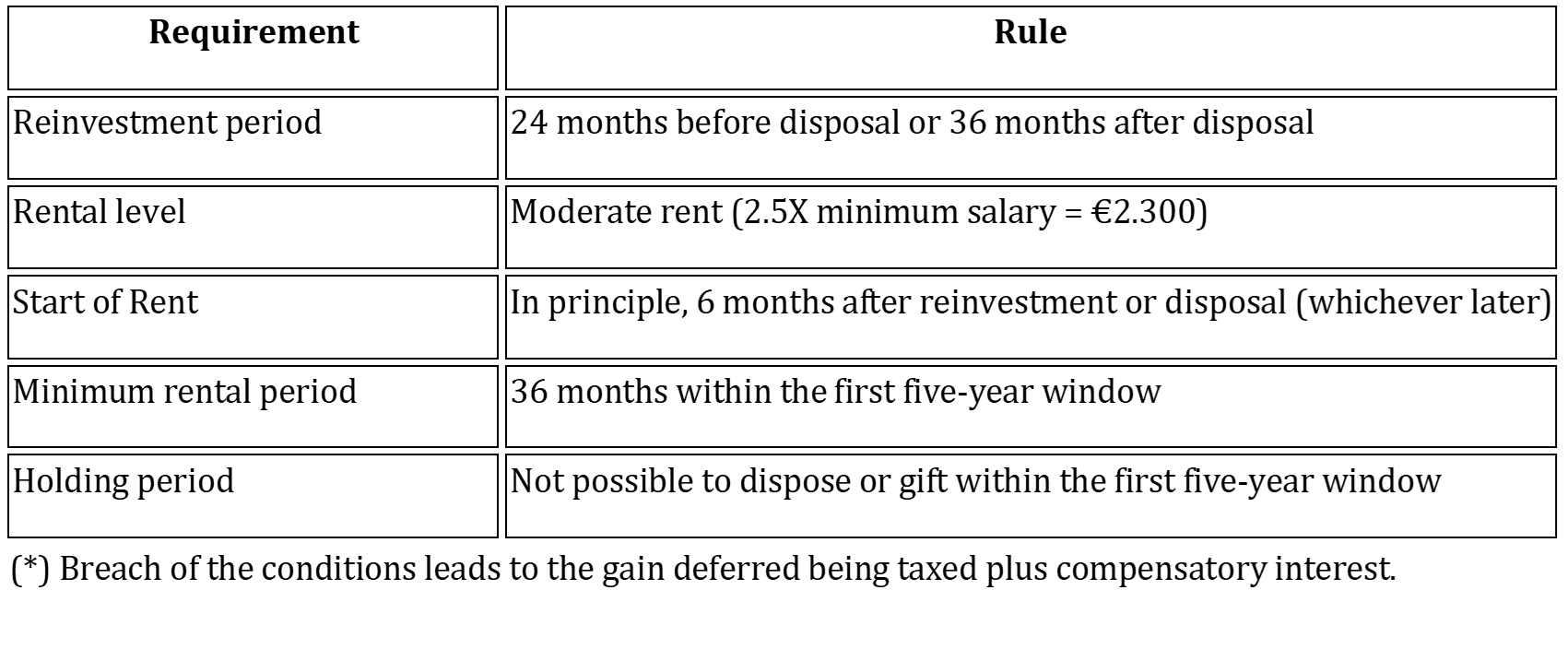

2. New Capital Gains Reinvestment Relief for Secondary Residences

A new reinvestment relief may apply where capital gains derived from the disposal of residential property are reinvested in qualifying residential rental property within moderate rent parameters. This measure is primarily relevant to owners of second homes in Portugal considering the disposal of such property

Key Conditions to apply Relief (*)

Case Study

Maria is a Portuguese tax resident and owns a second home in Portugal acquired several years ago for €200,000. In 2027, she sells the property for €500,000, generating a capital gain of €300,000, which would ordinarily be subject to Portuguese taxation.

Rather than paying tax on the gain, Maria reinvests the entire sale proceeds of €500,000 in the acquisition of two apartments intended for residential rental. The apartments are leased at monthly rents of €2,200 each, within the moderate-rent thresholds established by the new regime.

Provided all statutory conditions are satisfied, the €300,000 capital gain realised on the disposal of the original property may benefit from the reinvestment exemption. However, the exemption remains conditional. If Maria disposes of either apartment within five years of the reinvestment, increases the rent above the applicable threshold, fails to enter into a qualifying lease within the prescribed period, or does not satisfy the minimum rental requirements, the previously exempt gain may become taxable. In such circumstances, the tax would generally become due together with potential compensatory interest.

Kore Take

For many private clients, the relevant question is not whether the tax can be saved, but whether the expected after-tax return from the qualifying rental investment justifies the loss of flexibility and alternative investment opportunities (and their yield).

Kore Partners expects the practical application of this new regime to be relatively limited. While it may provide a valuable exemption for taxpayers disposing of second homes or investment properties, the relief is subject to extensive conditions and monitoring. Particular attention should be given to the fact that the exemption may be even clawed back, together with compensatory interest, if the statutory requirements cease to be satisfied.

The regime may be relevant both to non-residents disposing of Portuguese secondary homes and to Portuguese residents disposing of foreign residential property who reinvest in qualifying Portuguese rental property. Finally, the legislation only appears to recognise reinvestment in Portuguese residential property (differently from the rules of the main home). The absence of an equivalent relief for reinvestment in residential property located in another EU or EEA jurisdiction could also raise equal questions regarding compatibility with the free movement of capital.

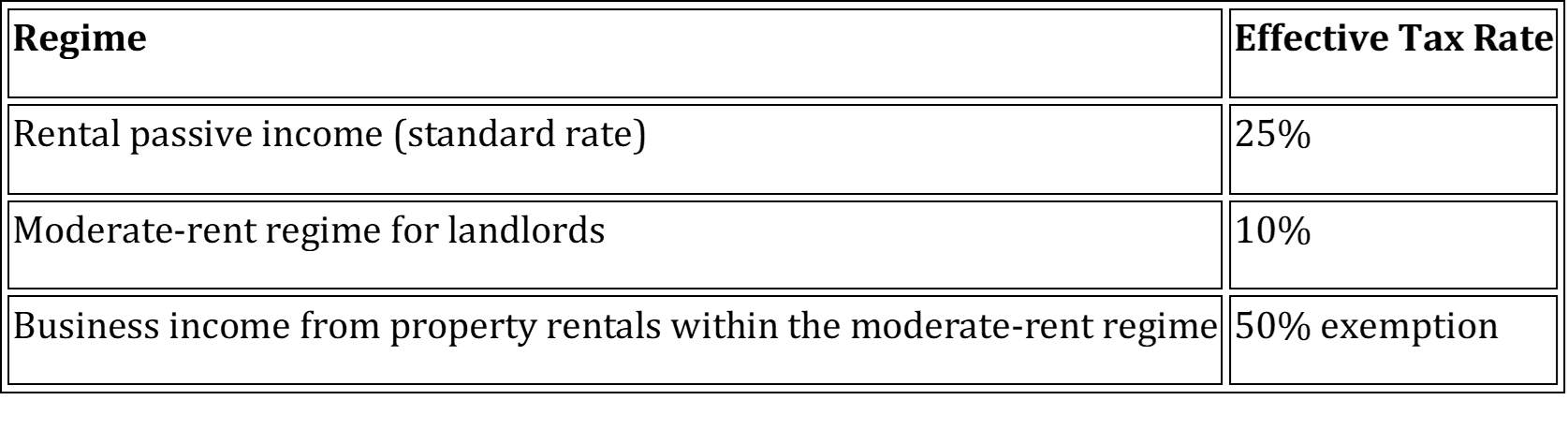

3. Reduced Taxation of Residential Rental Income

Landlords deriving rental income from qualifying moderate-rent residential leases (not exceeding approximately €2,300 per month) may benefit of a reduction of the effective income tax rate to 10%. For taxpayers with organised accounting and deriving business and professional income (including those operating via companies), rental income arising from qualifying moderate-rent leases may benefit from a 50% tax exemption.

Kore Take

The tax reduction to 10% for qualifying moderate-rent leases may improve the economics of long-term residential rentals and should be welcomed by landlords willing to operate within the applicable rent thresholds or by investors considering reinvestment into this segment of the market.

The extension of the benefit to taxpayers carrying on rental activities through an organised business structure (including companies) is also noteworthy. The 50% exemption applicable to business income derived from qualifying rentals may create an additional incentive for owners of short-term rental properties and local accommodation units to consider a transition to the long-term residential market. However, the practical attractiveness of the regime will ultimately depend on the level of the applicable rent caps and their impact on the expected rental yield.

4. VAT Incentives for Residential Construction

Another relevant measure is the extension of the 6% reduced VAT rate, instead of the standard 23% rate, to certain residential construction and rehabilitation projects.

For private clients, the measure is mainly relevant to:

residential properties intended for sale at moderate prices, currently up to approximately €660,000, for the purchaser’s own permanent residence; and

residential properties intended for long-term rental at moderate rents, currently up to approximately €2,300 per month.

The reduced VAT rate may apply to qualifying construction and rehabilitation works carried out in connection with these projects.

In addition, individuals constructing their own permanent residence may benefit from a VAT reimbursement mechanism where the reduced rate is not directly applied by contractors. Under this mechanism, part of the VAT paid may be recovered after completion of the project, subject to compliance with strict statutory requirements.

Kore Take

Although VAT represents a significant component of construction costs, the practical application of this measure may be limited for private clients, particularly in the main urban areas, due to the applicable value caps and the strict conditions attached to the regime. Investors and individuals undertaking construction or rehabilitation projects should carefully assess whether the moderate-price and moderate-rent limitations are compatible with the economics of the project before relying on the reduced VAT regime or the VAT reimbursement mechanism.

5. Other Changes

Extension of IMT Payment Deadline. The deadline for payment of IMT (Real Estate Transfer Tax) has been extended. The tax may now be paid either on the date of assessment or within the following 30 days. This measure provides additional flexibility for transaction planning, funding arrangements and completion processes.

New Accessible Rent Regime (RSAA). The new Simplified Accessible Rent Regime ("RSAA") replaces the former Affordable Rent Programme and seeks to simplify access to favourable tax treatment for residential rental activity. Amongst other benefits, qualifying rental income may benefit from full exemption from Personal Income Tax ("IRS") or Corporate Income Tax ("IRC"), subject to compliance with strict applicable conditions.

Housing Lease Investment Contracts (CIA). A new Housing Lease Investment Contract ("CIA") regime is introduced mainly for corporate investors entering into long-term housing investment agreements with the Institute for Housing and Urban Rehabilitation ("IHRU"). The regime is intended to encourage investment in the construction, rehabilitation and acquisition of residential property for long-term rental or residential subletting purposes at low rents, with contract periods of up to 25 years. The available incentives may include, among others: (i) exemption from IMT and Stamp Duty on acquisition of property; (ii) exemption from Municipal Property Tax ("IMI") for up to eight years and 50% reduction of IMI for the remaining duration of the CIA; (iii) application of the reduced 6% VAT rate to qualifying construction works; and (iv) reimbursement of 50% of VAT incurred on architectural, engineering, project and related technical services.

Kore Take

Although these measures may technically be available to private investors, their practical relevance is likely to be greater for institutional investors, developers and professionally managed residential rental platforms capable of structuring projects around the detailed requirements of the various regimes and regulatory commitments.

6. Action Points

While the housing package introduces several tax incentives, most of the benefits are accompanied by detailed eligibility requirements that limit it practical application and time frame limitations (in some cases up to 31 December 2029) putting further emphasis on the assessment of the economic and practical implications of each regime before relying on any of those tax benefits.

© Kore Partners, 2026

This briefing provides for general information and is not intended to be an exhaustive statement of the law. Although we have taken care to provide accurate information, this should not replace legal advice tailored to your specific circumstances. This briefing is intended for the use of clients and selected recipients. Queries or comments regarding this, including joining our mailing list, can be directed to kore@korepartners.com.